Can a 58-Year-Old With $2.4M Retire Today? The RIA Framework for Answering in One Meeting

DeepVest turns the hardest retirement question into a clear review of income, taxes, risk, spending, and sequence-of-return pressure.

By Amit Nar, Head of Client Success

Every advisor has heard some version of this question:

“Can I retire now?”

For a registered investment advisor, this question isn’t just about assets. It’s about spending, taxes, healthcare, Social Security, market timing, risk tolerance, behavior, and family goals.

One number can make the client feel safe. The wrong number can create false confidence, which is why retirement-readiness conversations need more than a rule of thumb. A 4% withdrawal rule or a Monte Carlo score can be useful, but they’re not enough. The advisor needs a client-ready framework.

Using DeepVest, a broad retirement question like this becomes a structured analysis an advisor can review, refine, and explain in one meeting.

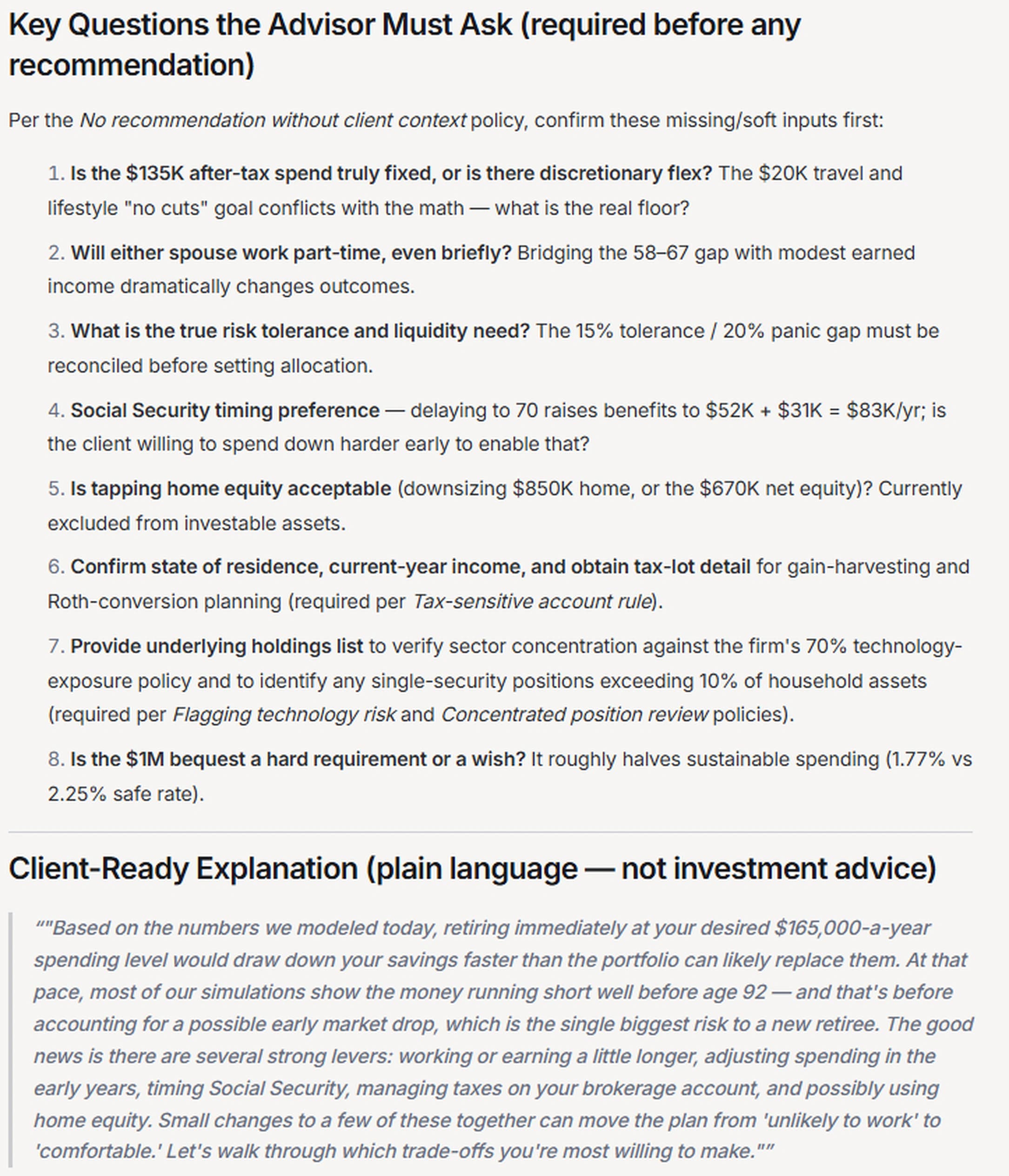

We Asked DeepVest AgentLab

We posed the following question to DeepVest AgentLab:

“I am a Registered Investment Advisor preparing for a client meeting. A 58-year-old client with $2.4M in investable assets asks, ‘Can I retire today?’ Use the synthetic client case below to build a concise retirement-readiness analysis with specific numbers: annual spending capacity, sustainable withdrawal rate, income gap, tax risks, healthcare/Medicare bridge risk, sequence-of-return risk, portfolio drawdown risk, and probability-style scenarios if possible.

Create an advisor-ready answer with: the top 5 issues to review, estimated dollar impact where possible, a table ranking each issue by urgency, key questions the advisor must ask before making a recommendation, and a simple client-ready explanation that is clear, professional, and not investment advice.”

We gave AgentLab a detailed synthetic client case to work from:

- Household: a 58-year-old client and a 56-year-old spouse, married, who want to retire immediately with $2,400,000 in investable assets.

- Accounts: $950,000 in a taxable brokerage, $1,050,000 in a traditional IRA and 401(k), $250,000 in a Roth IRA, and $150,000 in cash.

- Allocation: 58% U.S. equities, 12% international equities, 20% bonds, and 10% cash.

- Cost basis and taxes: a $720,000 cost basis on the $950,000 taxable account, about $230,000 of embedded unrealized gain, and a blended long-term capital gains rate near 23.8%.

- Spending: $135,000 of desired after-tax spending, roughly $165,000 gross, with a 3.0% inflation assumption.

- Income: a $275,000 current salary, no spouse income or pension, and Social Security of $42,000 for the client and $24,000 for the spouse at age 67, rising to $52,000 and $31,000 at age 70.

- Healthcare: about $24,000 per year in private premiums and out-of-pocket costs until Medicare begins at 65.

- Home and debt: an $850,000 home with a $180,000 mortgage ($2,400 per month, 8 years left), an $18,000 auto loan, and no credit card or student debt.

- Risk profile: moderate, comfortable with a 15% drawdown but likely to panic past 20%.

- Goals: retire now if realistic, keep the current lifestyle, budget $20,000 a year for travel in the first 10 years, leave at least $1,000,000 to the children, avoid running out of money, and reduce taxes where possible.

- Planning assumptions: life expectancy of 92 for the client and 94 for the spouse; a 5.5% base-case return, 3.5% bear case, and 7.0% strong case; and a sequence-of-return stress test of a 20% portfolio decline in year one.

AgentLab’s Response

Why This Matters for RIAs

The client wants a yes-or-no answer, but the advisor needs a real answer.

Manually, this can take hours. The advisor may need to rebuild the household balance sheet, estimate spending, model healthcare costs, test Social Security timing, calculate withdrawal rates, run sequence-risk scenarios, review tax trade-offs, and still translate the result into language the client can understand.

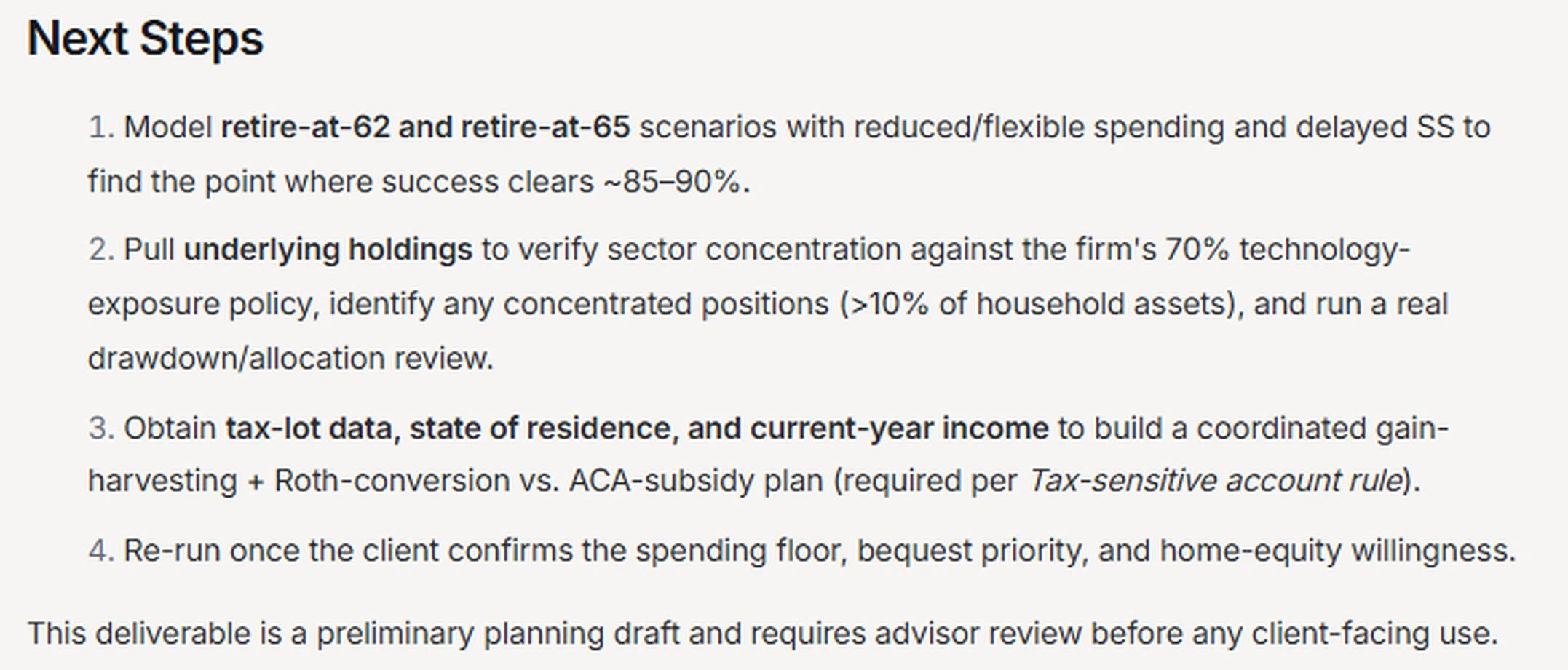

DeepVest compresses that work into a practical advisor workflow by:

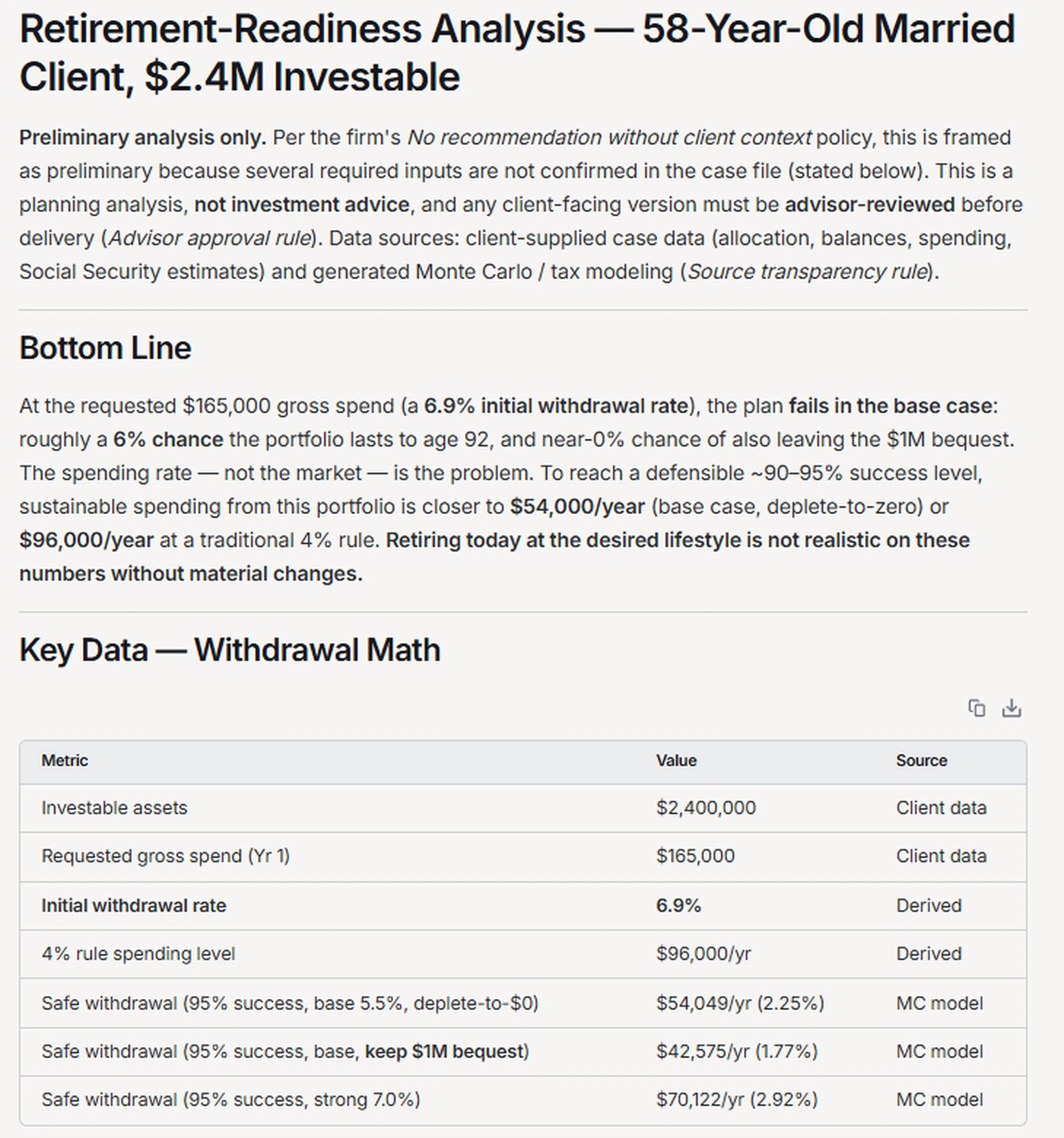

- Identifying the key number: a 6.9% withdrawal rate.

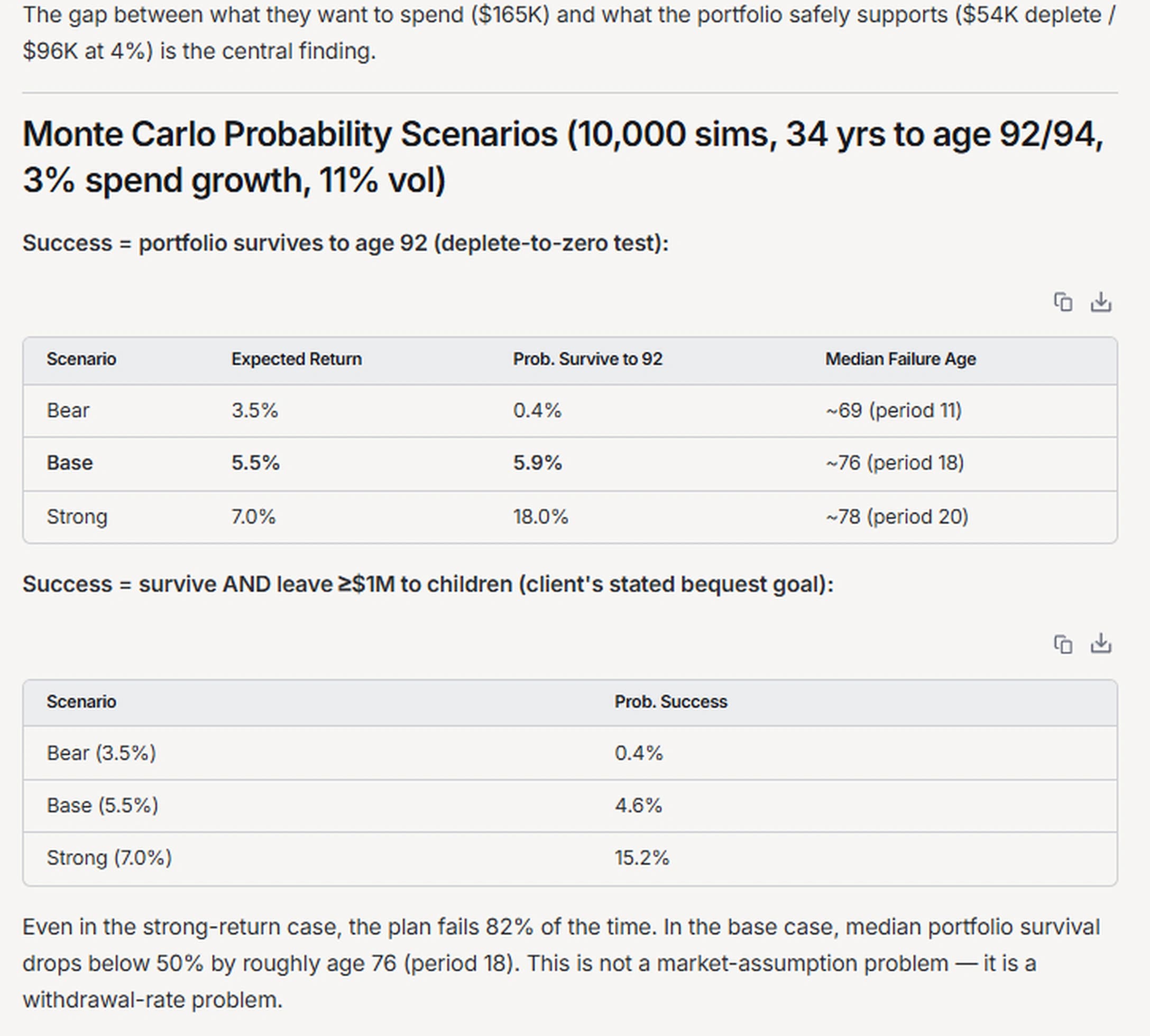

- Quantifying the risk: only 5.9% base-case survival.

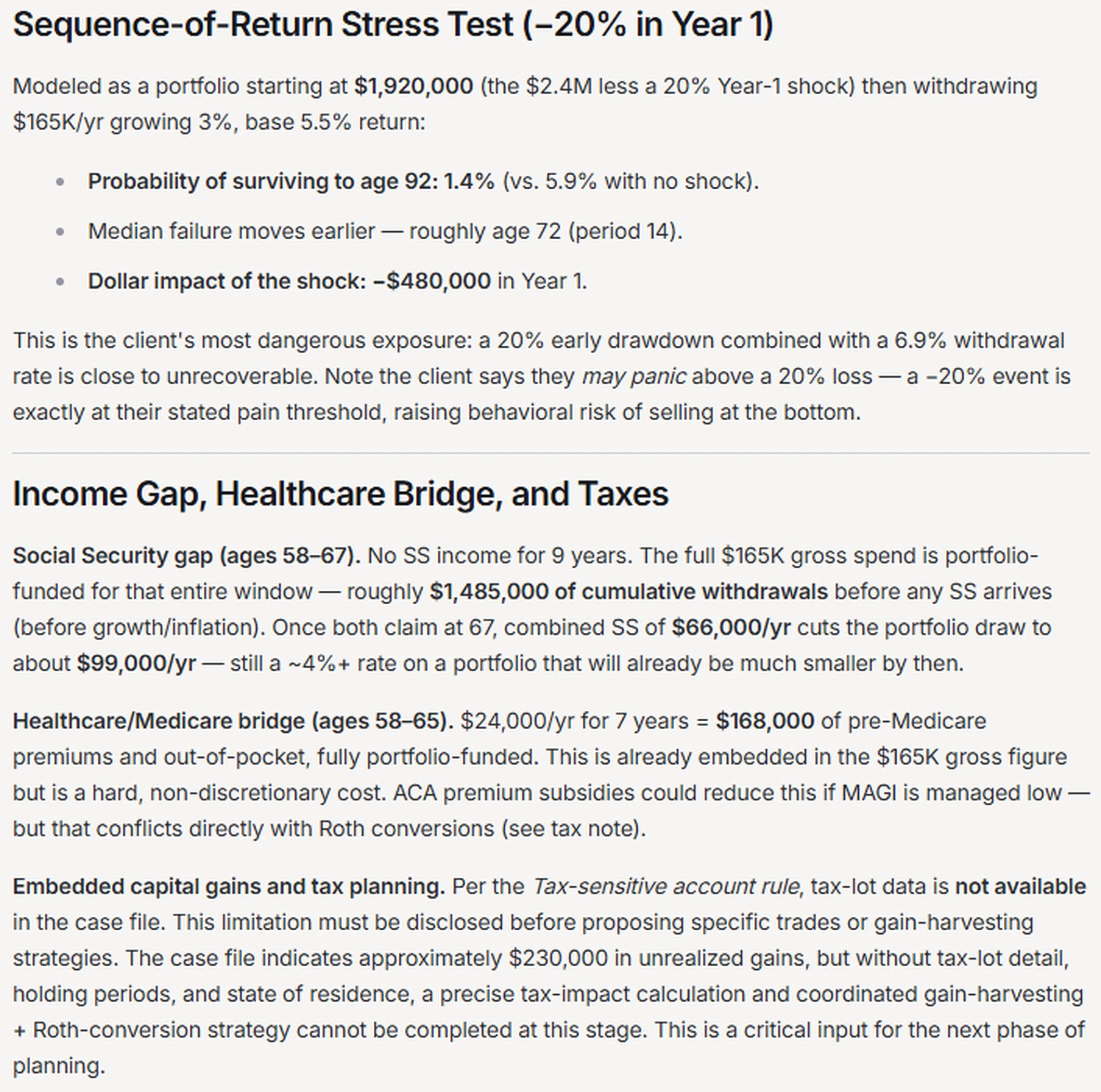

- Showing the shock: a 20% first-year decline cuts survival to 1.4%.

- Giving the advisor the meeting language.

The client gets a real answer. The advisor gets there in one meeting, not three weeks.

Schedule a demo with DeepVest to see how DeepVest helps RIAs run portfolio audits, identify hidden risks, and turn complex analysis into client-ready conversations.

Advisor Takeaway

The best advisors don’t answer retirement questions with hope. They answer with structure.

A client with $2.4 million may feel wealthy. But if the spending rate is too high, the plan can still fail.

DeepVest helps RIAs turn that lesson into a clear conversation: what works, what doesn’t, what needs to change, and what questions need to be answered before any recommendation.

This is the difference between answering a client and preparing an advisor.

Schedule a demo with DeepVest to see how DeepVest helps RIAs run portfolio audits, identify hidden risks, and turn complex analysis into client-ready conversations.

For questions, contact: [email protected].